Cover Story

Latest 2025 market developments and the outlook for 2026

A look at GlobalData’s sales analysis and forecasts by major global regions.

Powered by

Main image:

The latest forecast update from GlobalData has, once again, hinged on US international trade policy. Having made sizable cuts to the near-term outlook earlier in the year, GlobalData’s forecast is now more positive – though 2026 is seen as flat on 2025. Earlier this year, it was assumed that the 25% additional US import tariffs imposed on the auto sector would endure well into 2026.

However, agreements struck between the US and trade partners —the EU, Japan and Korea — where import tariffs are set at 15%, imply upward price pressure on US vehicles will not be as strong as feared. Furthermore, OEMs have, so far, not been pushing through price rises to US customers, with this supporting selling rates.

From a macroeconomic point of view, the outlook has also improved during the year. Global GDP is now forecast to grow by around 2.7% in 2025, confounding gloomier assessments earlier this year. A flurry of trade deals has helped, as has some frontloading of orders ahead of tariff deadlines, though, as with the light vehicle outlook, it is a more protectionist environment than at the start of the year.

Of the major markets, China stands out with double-digit YoY growth rates during the year, while the US has also managed to comfortably eclipse its 2024 level. On the other hand, Europe is a laggard, both in terms of being down against 2024 results, and more generally in that it remains well below its pre-pandemic levels.

China’s strong market performance is supported by several factors, including both government incentives and aggressive competition. The vehicle trade-in scrappage scheme has continued this year, while tax breaks on NEVs remain in place. Meanwhile, the vast number of brands and models competing for the attention of Chinese consumers ensures that the price war remains intense, heightening financial stress on companies operating in the sector. The government is pushing for a de-escalation in the price war to ensure stabilization of supply chains.

The Trump administration’s policy approach to trading partners added greater uncertainty for the US vehicle market’s 2025 outlook. However, OEMs have adopted a wait-and-see approach, such that vehicle transaction prices have not been cranked up, while deals coming through with trading partners are also helping to de-escalate pricing pressures moving forward.

Since our previous forecasts, the global LV market baseline forecast has increased markedly over the 2025-26 period as a result of two main considerations: 1) the aforementioned trading agreements reached between the US and its key trading partners; and 2) assumptions surrounding the government incentivization of the Chinese LV market. We now assume that the trade-in scheme in China will be extended once again, until the end of 2026. On a global basis, with rapid growth in 2026, the market will then broadly flatline in 2027 as China struggles from less government support and an easing in aggressive vehicle pricing, before sales will resume an upward trajectory later in the decade.

The last peak for the global light vehicle market saw it hit 94.5 million units in 2017, with a major downturn during the Covid 19 pandemic and supply shortages in semiconductors constraining the sales recovery across the world in subsequent years. In 2026, the global light vehicle market is forecast at 92.2 million units, flat on 2025’s estimated 92.4 million units.

Production outlook

Both the emergence of a better-than-expected global trading environment, and the assumption that the Chinese authorities plan to extend the auto trade-in subsidies for their domestic market, underpin a significant upward revision to GlobalData’s global light vehicle production forecast. The outlook now stands at 92 million units (+1.9% YoY) for 2025 and 93.6 million units (+1.7% YoY) for 2026.

New agreements with key trading partners, including Japan, Korea and the EU, have cut auto specific US import tariffs to 15% from the initial ‘shock-tariff’ of over 25% introduced in April 2025. This earlier-than-expected cut to the tariff level has helped to reduce the potential impact upon both vehicle and auto component import prices.

Combined with the wider use of USMCA tariff offset mechanisms and OEM cost absorption strategies, the demand-led production outlook for North America has been boosted by an annual average of 570k units in 2025 and 2026. Nevertheless, inventory control in the region remains tight as demand uncertainties prevail.

Slower-than-expected domestic demand in the key vehicle producing hubs of Japan and Korea has undermined their near-term production expectations. However, a more solid US-destined LV export outlook—following the recent trade agreements—is anticipated to provide some volume offset to the local demand weakness.

For China, much depends on the scrappage incentive and whether or not it is scrapped at the end of the year. It could be extended for another year, possibly operating at a lower subsidy level.

In Europe, intensifying competitive pressures in and from China, the stuttering electrification transition, and wider economic fragilities, all combine to undermine vehicle production output expectations in the near term.

The US

The US economy has shown surprising strength despite pressures like inflation and a cooling labour market. Second quarter US GDP growth was revised up from a 3% annualised rate to 3.8%, indicating stronger expansion than first reported. This improvement was largely driven by higher consumer spending, which is notable given the quarter’s sluggish job growth. The recent, extended US government shutdown, the longest on record at 43 days halted the release of major official economic reports. Meanwhile, several ground reports indicate that corporate profits have risen at their fastest clip in four years, contradicting expectations that the trade war would slow business performance nationwide.

The economy is growing with healthy GDP gains, but it still faces issues like persistently high inflation and a cooling labour market. Combining tariff increases with easier monetary policy could push inflation higher.

Inflation growth for 2025 is forecasted at 2.8%, with real GDP growth expected to be 1.8%.

Despite President Trump’s actions to create a playing field that is agnostic to propulsion type by removing incentives for plug-ins and diluting the CO2-reduction roadmap, the US LV BEV market hit new highs during the course of 2025. However, this was a false dawn, created by pull-forward of demand in advance of the termination of plug-in tax credits at the end of September. While there is some good news in that several OEMs have said they will fiscally support the plug-in sector by replacing the lost tax credits, this is probably not sustainable, and GlobalData has lowered its US electrification forecast significantly as a result.

In October, US light vehicle sales went fell by 4.3% to 1.28 million units.

GlobalData forecasts a broadly flat US light vehicle market for the next few years – at 16.1 million units in 2025 and 16.0 million units in 2026, as higher vehicle pricing and slower economic growth hold back a stronger performance.

Europe

The European market outlook remains firmly in contractionary territory for 2025. In Western Europe, three of the big five markets are set to fall short of their 2024 totals, with tough economic conditions a recurring theme. In France, slow economic growth is being compounded by an uncertain political backdrop.

The German economy is barely going to register an uptick this year, and as such LV sales there are likely to fall around 2%. A similar outlook for the year is expected for Italy.

The UK economy is far from a strong performer but will at least grow the right side of 1% this year, ensuring some growth for the car market, albeit modest. Support for BEVs has also been rolled out in the form of the government Electric Car Grant which should give a modest uplift to the market. The big winner among the West European markets is Spain, where a strong economy continues to translate into sizeable growth of both car and LCV sales.

In Eastern Europe, while strong, the Turkish market has not been able to make up for the slowdown in the Russian light vehicle market, with vehicle import taxes and borrowing costs among market headwinds.

In 2026, Europe’s light vehicle market is projected at 18.5 million units, in line with where it was in 2024 and just 1.4% ahead of the 2025 level.

Asia-Pacific

The Japanese market has been making YoY progress in 2025, though this if off a weak base due to market disruption from the Toyota/Daihatsu safety test rigging scandal. More supply-chain disruption earlier in the year has made way for rather disappointing light vehicle selling rates on a backdrop of weak economic growth.

Source: GlobalData

Nonetheless, the regional market should expand this year thanks to China. However, China’s market is forecast to be slightly down in 2026 as the price war winds down and that means the region’s market is constrained at around 43 million units. Upside risks to the market forecast include the development of solid-state NEV batteries and the appeal of greater range and faster charging times.

The ASEAN 2025 light vehicle sales outlook has been marginally increased to 3.12 million units, thanks to upward trends in Indonesia and Thailand. Additionally, the 2025 forecast carries upside risks, as demand in Malaysia and Thailand could be boosted by expectations of price hikes in 2026.

Source: GlobalData

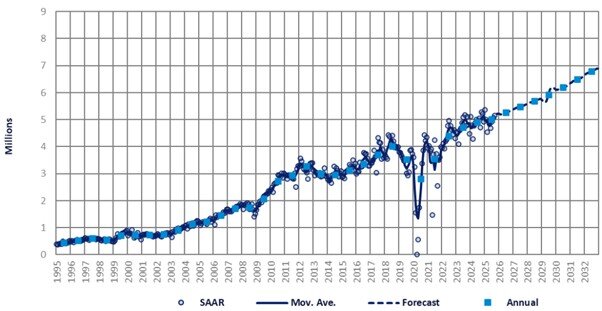

GST cuts and festive buying boost India’s vehicle market

India’s Light Vehicle (LV) wholesale figures for September increased by 15% month-on-month (MoM) to 437k units, with Passenger Vehicles (PVs) up by 16% to 373k units and Light Commercial Vehicles (LCVs) with a gross vehicle weight of up to 6T climbing by 10% to 64k units. On a year-on-year (YoY) basis, LV sales increased by 6%, supported by gains in both PVs and LCVs, which rose by 6% and 8%, respectively.

The MoM surge in PV wholesale volumes was driven by the early festive season (Navratri) and the implementation of new GST rates, which lowered car prices. Retail inflation eased to an eight-year low, contributing to positive consumer sentiment.

Demand is expected to rise in the fourth quarter following the GST rate cut on automobiles and household items, which should lower costs and increase disposable income. The ongoing festival season, combined with price reductions from lower GST rates and aggressive marketing, is also likely to further stimulate demand.

The market is expected to maintain a solid growth momentum through 2025 and 2026, supported by healthy domestic demand, improving supply stability, and new product launches. India LV sales are forecast at 5.0 million units in 2025 and 5.3 million in 2026. The long-term outlook through 2032 also remains robust, with LV sales reaching 6.8 million units. Solid demand prospects are also expected to continue to boost India’s automotive FDI.

India’s vehicle market on a strong upward trend. Credit: GlobalData